|

From: John Conover <john@email.johncon.com>

Subject: Quantitative Analysis of Non-Linear High Entropy Economic Systems I

Date: 14 Feb 2002 07:38:46 -0000

Much of applied economics has to address non-linear high entropy systems-those systems characterized by random fluctuations over time-such as equity prices, gross domestic product, industrial markets, etc.

An optimal wagering strategy for high entropy systems was first suggested by Claude Shannon in the mid 1940's in his pioneering work on information theory, The Mathematical Theory of Communication, (pp. 39-42.) The concept was further refined by J. L. Kelly Jr. in the Bell System Tech. J. vol. 35, 1956, A New Interpretation of Information Rate, (pp. 917-926), which established the isomorphism between the information-theoretic concept of information rate in a binary symmetric channel and speculation under uncertainty. More recently, Fazlollah M. Reza in An Introduction To Information Theory, (pp. 450-452,) has offered an alternative derivation that requires only the concepts of the law of large numbers, and the maxima from calculus-both taught in freshman mathematics-to derive the same optimal wagering strategy.

Note: the C source code to all programs used are available from the NtropiX Utilities page, or, the NdustriX Utilities page, and are distributed under License.

Following Reza, suppose a gambler wagers on an iterated game of

chance. Further, suppose there is a chance,

P, of the gambler winning any iteration

of the game, and of 1 - P, of

losing. Let the capital the gambler starts with be

V(0), and

V(t) the capital after the

t'th iteration of the game. Since the

gambler is not certain of the outcome of any iteration of the game,

only a fraction, f, of the capital is

wagered on each iteration of the game. Thus, after

t many iterations the capital is:

w l

V(t) = (1 + f) * (1 - f) * V(0) ..................(1.1)

where w is the number of times the

gambler won, and l = t - w, the number

of times the gambler lost. These numbers are functions of two random

variables, denoted by W and

L. Then, by the law of large

numbers:

1

lim - W = P .............................(1.2)

t->infinity t

1

lim - L = q = 1 - P .....................(1.3)

t->infinity t

The gambler must determine the fraction,

f, of the capital to wager on each

iteration of the game, which will maximize the average exponential

growth rate, G, of the capital, i.e.,

maximize the value of:

1 V(t)

G = lim - ln (----) .....................(1.4)

t->infinity t V(0)

with respect to f:

W L

G = lim - ln (1 + f) + - ln (1 - f) .....(1.5)

t->infinity t t

G = P ln (1 + f) + q ln (1 - f) ....................(1.6)

which, by taking the derivative with respect to

f, and equating to zero, is maximal

when:

dG P - 1 1 - P

-- = P (1 + f) (1 - f)

df

1 - P - 1 P

- (1 - P) (1 + f) = 0 ................(1.7)

and, combining terms:

P - 1 1 - P

P (1 + f) (1 - f)

P P

- (1 - P) (1 - f) (1 + f) = 0 ................(1.8)

and, splitting:

P - 1 1 - P

P (1 + f) (1 - f)

P P

= (1 - P) (1 - f) (1 + f) ....................(1.9)

Taking the logarithm of both sides:

ln (P) + (P - 1) ln (1 + f) + (1 - P) ln (1 - f)

= ln (1 - P) - P ln (1 - f) + P ln (1 + f) .....(1.10)

and combining terms:

(P - 1) ln (1 + f) - P (ln (1 + f) + (1 - P) ln (1 - f)

+ P ln (1 - f) = ln (1 - P) - ln (P) ...........(1.11)

or:

ln (1 - f) - ln (1 + f) = ln (1 - P) - ln (P) ......(1.12)

and performing the logarithmic operations:

1 - f 1 - P

ln (-----) = ln (-----) ............................(1.13)

1 + f P

and exponentiating:

1 - f 1 - P

----- = ----- ......................................(1.14)

1 + f P

reduces to:

P (1 - f) = (1 - P)(1 + f) .........................(1.15)

and expanding:

P - P f = 1 - P f - P + f ..........................(1.16)

or:

P = 1 - P + f ......................................(1.17)

and, finally:

f = 2 P - 1 ........................................(1.18)

Substituting, q, from Equation

(1.3) into Equation

(1.6):

G = P ln (1 + f) + (1 - P) ln (1 - f) ..............(1.19)

where G is

the average exponential growth rate of the gambler's capital, per

iteration of the game. As a useful form, exponentiating both

sides:

P (1 - P) G

g = (1 + f) (1 - f) = e ...................(1.20)

where the gain, g, is the average

multiplicative gain per iteration of the game, i.e., after

t many iterations, the gambler's capital

would have increased by a factor of

g^t.

|

As a side bar, if For the initiated, the equations can be derived using Ito

Calculus, which is the preferred methodology in Geometric

Brownian Motion analysis. From Ito's

Lemma, then the average, Which has the interesting implication, for the sum of many Geometric Brownian Motion trajectories, (for example, a portfolio, or GDP,) that the sum is not ergodic, in the sense of the time-average of the sum not being equal to the ensemble average, (the ensemble having a Log Normal distribution.) |

Equation

(1.18) and Equation

(1.20) are important. As a simple example, suppose each outcome of

an iterated game depends on a throw of a fair six sided die-if the die

comes up four, or less, the gambler wins what was wagered; else loses

it. The gambler's optimal strategy is to put 1 /

3 of the capital at risk, (by wagering it,) on each

iteration of the game, since P = 4 / 6,

and from Equation

(1.18), f = 2 P - 1 = 1 / 3. The

gambler's capital would increase, from Equation

(1.20), on average, by a factor of g =

1.05826736798 per iteration of the game, or about

6% per game.

But how does the gambler play the game if the value for P is unknown?

Equation (1.20) offers a metric methodology. For the

t'th iteration of the game, the

fractional gain, f(t), in the gambler's

capital for the iteration is:

V(t) - V(t - 1)

f(t) = --------------- .............................(1.21)

V(t - 1)

The absolute value of f(t) is the

fraction of the capital the gambler wagered on the

t'th iteration of the game-it is the

fraction of capital that the gambler put at risk,

f. The capital increased if the gambler

won on the game in the t'th iteration,

and decreased if the gambler lost-by the fraction of the capital the

gambler put at risk, f.

|

As a side bar, this is one of the fundamental concepts in the

quantitative analysis of high entropy economic systems-risk is

the root-mean-square, This presents a definition issue for the term root-mean-square:

The term root-mean-square is used here in the engineering or

physics sense of noise power from electronic

communication theory; instantaneous power depends on the

absolute value of a quantity, (like

There is a potential conflict of definition between this

derivation and the concept of (implicit,) risk = statistical

root-mean-square, For the initiated, the running average of the marginal

increments, |

If n has a sufficiently

large data set size, then by the law of large numbers, in

n many iterations of the game, the total

number of wins for the gambler would be expected to be n

P and the total number of losses would be expected to

be n (1 - P), for an average number of

wins of (n P - n (1 - P)) / n = 2 P -

1. The average gain, avg

would then be:

avg = (2 P - 1) f ..................................(1.22)

where f is the return on the fraction

of capital wagered on each iteration of the game,

(srms,) and is equal to

rms, the root-mean-square of the

marginal increments of the capital, and

avg is the mean of the marginal

increments of the capital. Solving for

P:

avg

--- = 2 P - 1 ......................................(1.23)

rms

avg

--- + 1

rms

P = ------- ........................................(1.24)

2

The interpretation of P is that it is

the likelihood of up movement in the characteristics of a high entropy

economic system.

Substituting Equation

(1.18) for P in Equation

(1.24), and letting f = rms:

avg

---- + 1

rms + 1 rms

------- = -------- ................................(1.25)

2 2

or, maximal growth occurs when:

2

avg = rms .........................................(1.26)

|

As a side bar, note that the entropic model used is non-linear; it is not a random walk model. A random walk is a cumulative sum of a random variable-the noise is additive. In the entropic model used, the noise is multiplicative. The long term characteristics of the model exhibit a log-normal distribution, as mentioned in Section II. As an equivalent model, the iterative equation: can be used, where Note the similarity to the simplist non-linear dynamical system function, the iterated parabolic/logistic function: The paradigm of the model is that the higher order terms, (of which their may be many,) of the economic non-linear dynamical system can be modeled with a high entropy stochastic methodology-if the complexity of the economic system is sufficiently high. A concept not unlike pertubation theory. |

The concept is similar to automating risk

arbitrage, based on historical performance, where an

expected-value table of the difference between an

investment's potential upside, (multiplied by the probability

of achieving the potential upside,) and the the potential

downside, (multiplied by the probability of the downside

occurring,) is the expected value of the return of the

investment-the difference between the potential upside and potential

downside corresponding to the root-mean-square,

rms, of the value of the investment, and

the average, avg, the expected value,

where P is the likelihood of the

potential upside occurring.

Reiterating the important equations for high entropy economic systems:

avg

--- + 1

rms

P = ------- ........................................(1.24)

2

P (1 - P)

g = (1 + rms) (1 - rms) ....................(1.20)

and for maximal growth:

rms = 2 P - 1 ......................................(1.18)

which is when:

2

avg = rms .........................................(1.26)

where avg is the mean, and

rms the root-mean-squre, of the system's

marginal increments.

Of interest is that only two

variables,avg and

rms, are involved in optimizing the

performance of a high entropy economic system. Typical values for

avg and

rms are

0.0004 and

0.02, respectively, for daily

data. P would then have a value of

0.51, and

g a value of

1.0002 per day, which is about

5% per calendar year, for

253 business days in a calendar

year.

As an emperical exercise to demonstrate the usage of Equation

(1.24) and Equation

(1.20), the equity price history for General Electric, (ticker

symbol, GE,) for the last 10,103 days, (January 4, 1962, to February

15, 2002,) was downloaded from Yahoo!'s Historical Prices database, and

the csv2tsinvest

program used to convert the database to a time series. The mean of the

marginal increments of the price, avg,

and the root-mean-square of the price,

rms, was found to be

0.000499, and

0.015145, respectively, using the

tsfraction,

tsavg,

and, tsrms

programs. On January 4, 1962, the initial value of the equity was

$0.761300, adjusted for splits. On

February 15, 2002, the value was

$37.11.

From Equation (1.24):

0.000499

-------- + 1

0.015145

P = ------------ = 0.516474084 .....................(1.29)

2

And, from Equation (1.20):

0.516474084

g = (1 + 0.015145) *

(1 - 0.516474084)

(1 - 0.015145)

= 1.00779357225 * 0.992648138

= 1.00038441336 ..................................(1.30)

|

|

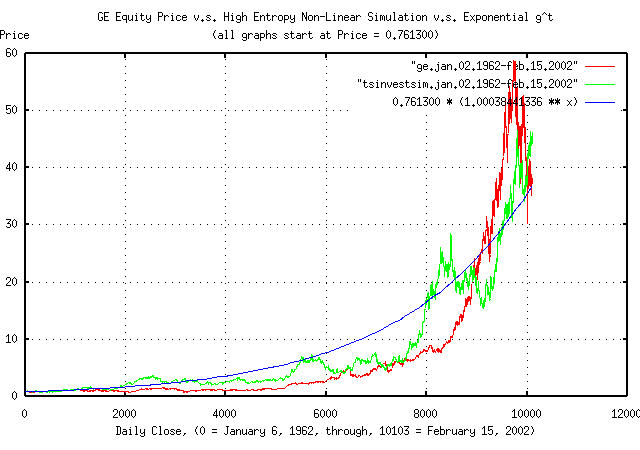

Figure I is a plot of the GE's equity price, from January 4, 1962,

to February 15, 2002, and the equation 0.761300 *

1.00038441336^t. Additionally, the tsinvestsim

program was used to generate a time series with the same

characteristics, (P = 0.516474084,

I = 0.761300, and f =

0.015145,) using a uniformly distributed random number

generator, to produce a binomial frequency distribution with 10103

elements to simulate a normal/Gaussian distribution, which is

overlayed, also.

|

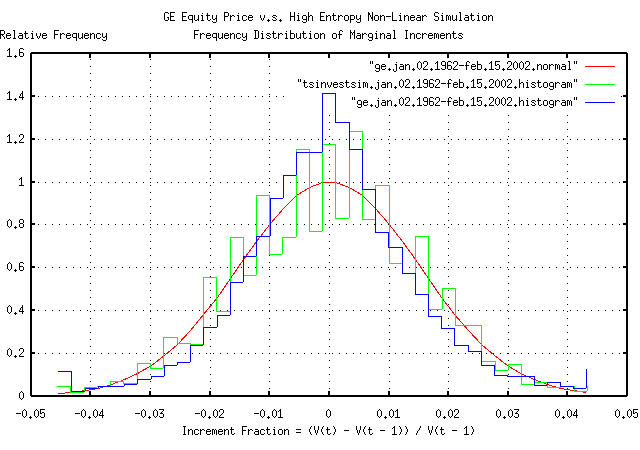

Figure II is the frequency distribution of the marginal increments

of GE's equity price, from January 4, 1962, to February 15, 2002, and

a least squares fit of the distribution to a Normal/Gaussian bell

curve distribution. The binomial frequency distribution of the

marginal increments of the time series simulated with the

tsinvestsim

program shown in Figure I is also displayed. The data in Figure II was

made with the tsnormal

program. The comb effect in the binomial frequency

distribution was caused by aliasing between the binomial elements in

the frequency distribution and the histogram element size of the plot,

and could be removed by choosing a larger histogram element size. Of

passing interest is the leptokurtosis in the frequency distribution of

the marginal increments of GE's equity price, which is explored

further in Example

III.

|

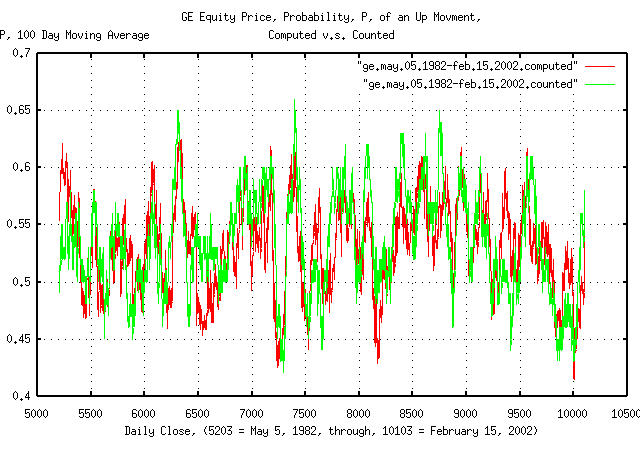

Figure III is a plot of the likelihood,

P, of an up movement in GE's equity

price as computed by the tsshannonwindow

program for a 100 day moving window, from May 5, 1981 to February 15,

2002-4,900 business days for clarity. The first time series presents

likelihood, P, computed by Equation

(1.24) for the moving window. The second by counting the number of

up movements in the window.

|

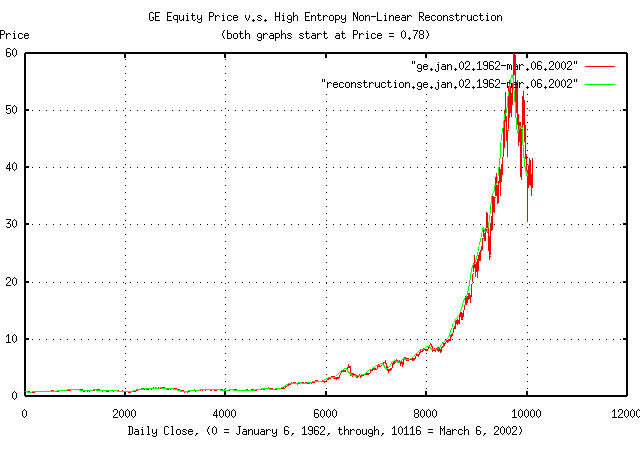

Figure IV is a plot of the reconstructed GE equity price time

series, as computed by the tsgainwindow

program for a 100 day moving window, from January 6, 1962 to March 6,

2002, overlayed on the original GE equity price. The tsgainwindow

program uses Equation

(1.24) and Equation

(1.20) to derive the statistics of the time series for the moving

window, which is then used for the reconstruction:

tsgainwindow -w 100 ge.jan.02.1962-mar.06.2002 | tsmath -l | tsintegrate | \

tsmath -e | tsmath -m 0.78 > reconstruction.ge.jan.02.1962-mar.06.2002

where "tsmath

-l | tsintegrate

| tsmath

-e | tsmath

-m 0.78" implements the geometric

reconstruction by taking the natural logarithm of the series,

integrating it, exponentiating it, and scaling it by a factor of 0.78,

which was the initial value of the original time series.

If the component companies in the DJIA are the premier companies in the US exchanges, then their equity price characteristics should be near optimally maximal, i.e., consistent with Equation (1.26).

| Symbol | Name | avg |

rms |

rms^2 |

|---|---|---|---|---|

AA |

Alcoa |

0.000510 |

0.020365 |

0.000415 |

AXP |

American Express |

0.000538 |

0.021724 |

0.000472 |

BA |

Boeing |

0.000493 |

0.024889 |

0.000619 |

C |

CitiGroup |

0.000405 |

0.022257 |

0.000495 |

CAT |

Caterpillar |

0.000423 |

0.019186 |

0.000368 |

DD |

Du Pont |

0.000331 |

0.017290 |

0.000299 |

DIS |

Disney |

0.000919 |

0.025126 |

0.000631 |

EK |

Eastman Kodak |

0.000338 |

0.028620 |

0.000819 |

GE |

General Electric |

0.000512 |

0.015452 |

0.000239 |

GM |

General Motors |

0.000257 |

0.017700 |

0.000313 |

HD |

Home Depot |

0.000818 |

0.027398 |

0.000751 |

HON |

Honeywell |

0.000438 |

0.020541 |

0.000422 |

HWP |

Hewlett-Packard |

0.001378 |

0.051051 |

0.002606 |

IBM |

International Business Machines |

0.000321 |

0.016877 |

0.000285 |

INTC |

Intel |

0.001406 |

0.028905 |

0.000835 |

IP |

International Paper |

0.000359 |

0.018274 |

0.000334 |

JNJ |

Johnson & Johnson |

0.000703 |

0.016049 |

0.000258 |

JPM |

JP Morgan Bank |

0.000375 |

0.023279 |

0.000542 |

KO |

Coca Cola |

0.000534 |

0.016808 |

0.000283 |

MCD |

McDonalds |

0.000506 |

0.020492 |

0.000420 |

MMM |

Minnesota Mining and Manufacturing (3M) |

0.000378 |

0.014766 |

0.000218 |

MO |

Philip Morris |

0.000770 |

0.017934 |

0.000322 |

MRK |

Merck |

0.000583 |

0.015963 |

0.000255 |

MSFT |

Microsoft |

0.001593 |

0.026458 |

0.000700 |

PG |

Procter and Gamble |

0.000515 |

0.015394 |

0.000237 |

SBC |

SBC Communications |

0.000597 |

0.016261 |

0.000264 |

T |

AT&T |

0.000113 |

0.022534 |

0.000508 |

UTX |

United Technologies |

0.000588 |

0.018409 |

0.000339 |

WMT |

WalMart Stores |

0.001507 |

0.034505 |

0.001191 |

XOM |

Exxon Mobil |

0.000479 |

0.013938 |

0.000194 |

TABLE I contains the average, avg,

the root-mean-square, rms, and the

root-mean-square, squared, rms^2, of the

marginal increments for the equity price time series for each of the

component companies in the DJIA. The daily close equity price history

for each component company in the DJIA was downloaded from Yahoo!'s Historical Prices database, and

the csv2tsinvest

program used to convert the database to a time series. The

tsfraction,

tsavg,

and, tsrms

programs were used to calculate the average,

avg, and, the root-mean-square,

rms, of the marginal increments of each

time series. The tsmath

program was used to square the rms

values. The time series files represented from between January 2, 1962

and July 9, 1986 for the various component companies, to March 6, 2002.

|

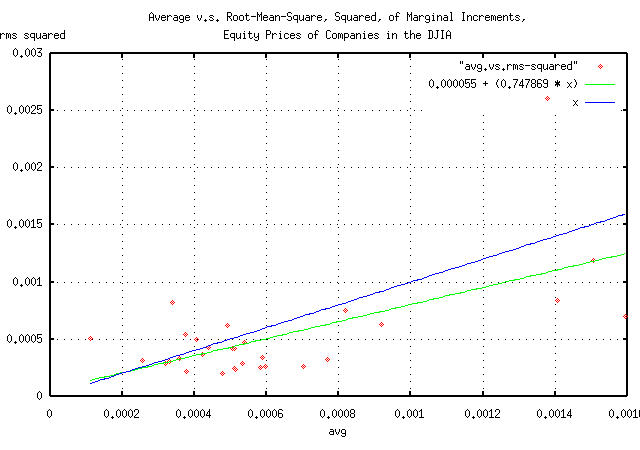

Figure V is a parametric scatter plot of the average v.s. the

root-mean-square, squared, avg and

rms^2, respectively, of the component

companies of the DJIA. The figure is a pictographic representation of

the data in TABLE I.

It does, indeed, appear that the equity price growth of most of the DJIA component companies is near optimally maximal, although slightly risk adverse.

The historical time series of the DJIA's 27949 daily closes, from

January 2, 1900 through March 6, 2002, inclusive, was obtained from Yahoo!'s database of equity Historical Prices, (ticker symbol

^DJI,) in csv format. The csv format was

converted to a Unix database format using the csv2tsinvest

program, filename

djia1900-2002, and files of the

marginal increments of the DJIA made:

tsfraction djia1900-2002 | tsnormal -t > djia.1900.jan.02-2002.mar.06

tsfraction djia1900-2002 | tsnormal -t -f > djia.1900.jan.02-2002.mar.06.histogram

From Figure

IV, the average and root-mean-square values, avg =

0.0004, and, rms = 0.02,

respectively, seem reasonable approximations for the median values for

the marginal increments of the equities in the DJIA. Additionally, the

instantaneous values of the equities in the DJIA seem to have a, from

Section

II, a log-normal distribution with a range that is, approximately,

an order of magnitude and a half. As a simple simulation of the DJIA,

the tsinvestsim

program can be used with the data

file:

tsinvestsim -n 1000 data 27949 | tsinvest -i -j | cut -f1 | \

tsfraction | tsnormal -t > tsinvestsim.jan.02.1900-mar.06.2002

tsinvestsim -n 1000 data 27949 | tsinvest -i -j | cut -f1 | \

tsfraction | tsnormal -t -f > tsinvestsim.jan.02.1900-mar.06.2002.histogram

and the files plotted:

|

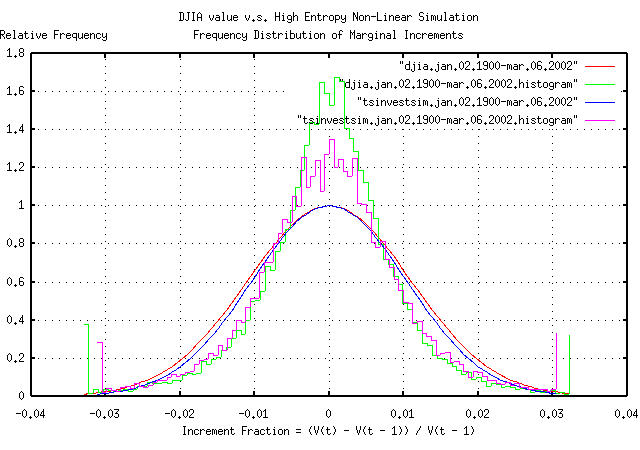

Figure VI is the frequency distribution of the marginal increments

of the DJIA's value, from January 2, 1900, to March 6, 2002, and a

least squares fit of the distribution to a Normal/Gaussian bell curve

distribution. The binomial frequency distribution of the marginal

increments of the time series simulated with the tsinvestsim

program. The data in Figure VI was made with the tsnormal

program.

|

As a side bar, Figure VI is interesting-the simulation was made using a binomial process, which produces normal/Gaussian distributions. The evolution of a geometric progression of a random variable with a normal/Gaussian distribution is a log-normal distribution. What happens is that the price distribution of the 30 equities in the DJIA evolves into a log-normal distribution, with one equity dominating the index value at all times; its price fluctuations dominate the fluctuations in the index, too. The contribution of the marginal increments of the other 29 equities contribute less to the index's fluctuations. So, it would be expected that an index, made up of the sum of equities from a geometric process, with price fluctuations that have a normal/Gaussian distribution, would have a bell curve that is pushed up around the mean with fat tails-exactly what is shown in Figure VI. (As a modeling exercise, slightly exponentiating normal/Gaussian distributed increments will simulate leptokurtosis, too.) Most economic time series exhibit such phenomena, and because of the importance, log-normal distributions will be discussed in Section II in some detail. Note that leptokurosis means higher risk; the tails contain

too much of the distribution and the root-mean-square,

In some sense, the long term objective of portfolio management is to minimize leptokurtosis in the increments of the portfolio's value; portfolios with leptokurtotic distributions of the increments gain fabulous wealth quite quickly, only to to lose it all when the risk asserts itself-a portfolio with leptokurtotic distribution of the increments can not remain a fugitive from the laws of probability forever. (Its why investing in indices is probably not such a good idea, and why the dot-com valuations came down so fast, too-the dot-com companies were notorious for having leptokurtotic distributed price fluctuations.) (Just so there is no confusion, Figure VI does not represent a log-normal distribution-it represents the sum of geometric processes that evolves into a log-normal distribution. Equity prices evolve into log-normal distributions, with, approximately, normal/Gaussian distributed increments; indices are the sum of equity prices, and have non-Gaussian distributed increments, i.e., distributions with fat tails, or leptokurtosis. As a final qualification, the amount of leptokurtosis is not stable, or constant over time-the long term evolution of indices with log-normal distributions of the constituent parts is for one part to totally dominate the index, and, in the long term, the marginal increments of the index will have the normal/Gaussian distribution of that part.) |

It has been suggested that the leptokurtosis in economic time series is created by the fractal dimension of the data not being 2- which is the value for a simple Brownian motion fractal-and persistence, (i.e., a slight tendency for the next movement in the time series to be like the last.) But there can be other reasoning, too.

tsmath -l djia1900-2002 | tslsq -o | tsroot -l | \

tsscalederivative > djia.1900.jan.02-2002.mar.06

tsinvestsim -n 1000 data 28048 | tsmath -l | tslsq -o | tsroot -l | \

tsscalederivative > tsinvestsim.jan.02.1900-mar.06.2002

where the data

file is the same as used for Figure

VI, above.

|

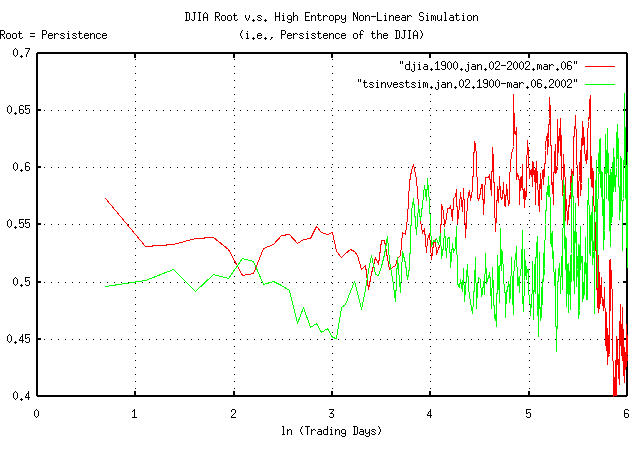

Figure VII is a plot of the persistence, (sometimes called the Hurst Exponent from rescaled range analysis, Range/Scale,) of the DJIA, and a simulation with similar statistics. Of interest is the variability of the persistence-it is far from constant over time, which would be expected in a well behaved fractal. Some observations:

The persistence of the DJIA at e^0.693147 =

1 day is 0.573078, and

then falls rapidly-this is a contradiction with the Efficient

Market Hypothesis, (EMH), which predicates that the market

responds to information instantaneously; the contradiction is not

serious for most analysis, and the approximation used in the EMH is

probably reasonable for general purposes, (all it says is that an

instantaneous market response to new information means

within a few days.)

At about e^2.2 = 9 days, the

persistence drops to just over 0.5.

And then the persistence raises to about 0.6 through the rest

of a calendar year, (of about 253 trading days in a calendar year,

or at ln (253) = 5.5, when it, quite

quickly, goes anti-persistent.

Although such variability in persistence could be attributed to Non-Linear Dynamical System, (NLDS,) dynamics, it is more likely a structural artifact. For example, the anomaly could be created by a downtrend, followed by an uptrend about 30 trading days later, on average, that happens, on average, about once a year, (in addition to the short term few day inefficiency.) Looking at the time series of the DJIA, October and November frequently have about a month and a half downward spike, which also happens to correspond with October 31, the time that mutual fund capital and income gains taxation liabilities are executed at the end of the fiscal year, as mandated under US Federal law, (usually, resulting in mutual fund companies holding a fire sale on equities they hold with bad pro forma.) Note, also, that many NLDS methodologies would indicate that structural phenomena are system dynamics-leading to inappropriate interpretations of the data.

However, using an average persistence of

0.57 for the DJIA, (and its constituent

equities, too,) can adequately model the NLDS/structural

phenomena. This means that the root-mean-square of the marginal

increments, rms, would not be added as

((1 / n) * sum increment^2)^0.5, but as

((1 / n) * sum increment^(1 /

0.57))^0.57. (For an example of the consequences of

assuming that risk is represented as the root-mean-square of the

marginal increments, see the section on the DJIA,

from Section

III.

Of passing interest is the fact that, as shown in Figure VII, the simulation showed substantial leptokurtosis, but no persistence.

As a approximation for non-linear high entropy economic system's

daily data, from Equation

(1.20), the exponential marginal gain per unit time,

g, will typically be about

1.0002, and the ln

(1.0002) will be about

0.0002. The average of the time series'

marginal increments, avg, that has

exponential marginal gain per unit time, g =

1.0002 will be about

0.0004. So, as an approximation, divide

the avg by two, and that's the

ln (g); add unity to get

g.

If a non-linear high entropy economic system is assummed to be operating near optimality-a reasonable assumption for most economic systems-then substituting Equation (1.26) into Equation (1.24):

avg

---- + 1

rms rms + 1 sqrt (avg) + 1

-------- = ------- = -------------- ...............(1.31)

2 2 2

-- John Conover, john@email.johncon.com, http://www.johncon.com/